Top Altcoins to Buy Before the Next Market Surge

The post Top Altcoins to Buy Before the Next Market Surge appeared first on Coinpedia Fintech News With the crypto market showing signs of renewed bullish momentum, investors are looking to position themselves before the next major rally. While Bitcoin and Ethereum often lead the […]

Sponsored

Crypto Pro Who 500x’d on PEPE Says This Coin Is the Next Big Thing—And It’s Launching Now!

The post Crypto Pro Who 500x’d on PEPE Says This Coin Is the Next Big Thing—And It’s Launching Now! appeared first on Coinpedia Fintech News A seasoned crypto expert, renowned for turning a remarkable profit on PEPE, now points to the next coin with explosive […]

Sponsored

The 5 Most Talked-About Cryptos of Q1 2025, Are You Holding Them?

The post The 5 Most Talked-About Cryptos of Q1 2025, Are You Holding Them? appeared first on Coinpedia Fintech News Rexas Finance (RXS) has emerged as the leading topic in crypto circles in Q1 2025, overshadowing even long-established tokens. Its unique value proposition in real-world […]

Sponsored

How to sell crypto via MetaMask: A beginner’s guide to cashing out

Key takeaways Not all tokens can be sold immediately. Airdropped or obscure tokens may lack liquidity or could be scams, so it’s important to check before attempting to cash out. Swapping and bridging may be required. To sell, you might need to convert tokens to […]

Analysis

Key takeaways

-

Not all tokens can be sold immediately. Airdropped or obscure tokens may lack liquidity or could be scams, so it’s important to check before attempting to cash out.

-

Swapping and bridging may be required. To sell, you might need to convert tokens to ETH or stablecoins and bridge them to the Ethereum mainnet.

-

MetaMask integrates fiat off-ramps. You can use the MetaMask Portfolio to sell ETH directly, but be prepared for KYC with third-party providers.

-

Non-KYC and P2P options exist. Platforms like Bisq or LocalCoinSwap allow trading without ID, but they carry more risk and require caution.

Not all tokens can be sold immediately. Airdropped or obscure tokens may lack liquidity or could be scams, so it’s important to check before attempting to cash out.

Swapping and bridging may be required. To sell, you might need to convert tokens to ETH or stablecoins and bridge them to the Ethereum mainnet.

MetaMask integrates fiat off-ramps. You can use the MetaMask Portfolio to sell ETH directly, but be prepared for KYC with third-party providers.

Non-KYC and P2P options exist. Platforms like Bisq or LocalCoinSwap allow trading without ID, but they carry more risk and require caution.

There are plenty of ways you might end up with a mix of different cryptocurrencies sitting in your MetaMask wallet.

Maybe you work in Web3 — as a developer, copywriter or designer — and your client paid you in their project’s native token.

Or maybe you’re part of a Bitcoin mining pool and occasionally receive rewards straight to your wallet.

You could be farming yield in decentralized finance (DeFi), earning annual percentage yield (APY) on your locked assets. Or, perhaps the most straightforward of all: You completed a few SocialFi tasks and received some community tokens via an airdrop.

Whatever the case, you’ve got crypto in your MetaMask — and now you want to turn it into cash.

In this guide, you’ll learn all the ways you can sell your crypto and withdraw the funds to your bank account or even in cash — whether you’re going through official Know Your Customer (KYC) channels or sticking to more private, non-KYC routes.

Things to know before selling tokens on MetaMask

Before you can turn your tokens into cash, there are a few things you need to get sorted in MetaMask because “not all tokens are created equal.” It’s not always as simple as hitting a “sell” button — especially if you’ve just received tokens via an airdrop or from a lesser-known project.

1. Why some airdropped tokens can’t be sold (yet)

Just because a token shows up in your wallet doesn’t mean it’s ready to be sold. In fact, many airdropped tokens aren’t listed on exchanges at all. That means there’s no market where you can sell them — not yet, anyway. You might see a price attached to the token, but without buyers or liquidity, that value isn’t something you can actually realize right now. So, while it’s great to receive free tokens, they may end up sitting idle in your wallet for a while.

Did you know? If you see a “100% sell fee detected” warning on a token, it’s likely a scam. Scammers airdrop these tokens, hoping you’ll try to sell or interact with them. But when you do, the smart contract takes the full amount — leaving you with nothing. Worse, some link to fake decentralized applications (DApps) that ask you to “claim” or “unlock” the tokens. Connecting your wallet or signing a transaction there can let scammers drain your real assets.

2. Adding missing tokens to your wallet

Sometimes, you’ll receive tokens that don’t even show up in MetaMask at first. That doesn’t mean they’re not there — it just means MetaMask doesn’t recognize them by default. You’ll need to add them manually by grabbing the token’s contract address (usually from the project’s official site or Etherscan) and importing it into your wallet. Once you do that, your balance will show up properly.

Similarly, if you want to receive any asset other than Ether (ETH), the “Import Tokens” option lets you manually add these missing tokens so they show up in the assets list.

3. Getting ready to swap or bridge

Even if your tokens are visible in MetaMask and technically have value, that doesn’t always mean you can sell them for cash right away. Many smaller or newer tokens don’t have direct fiat trading pairs — so you won’t be able to exchange them straight into dollars or euros.

To get around this, you’ll usually need to swap them for something more liquid, like ETH or a stablecoin such as USDC (USDC), which are more commonly supported by fiat off-ramps.

In some cases, your tokens might also be sitting on a different blockchain — like Arbitrum, BNB Chain or Polygon — while most fiat withdrawal options only support Ethereum mainnet. When that’s the case, you’ll need to bridge your tokens over to Ethereum before you can sell them.

One way to handle both of these steps — swapping and bridging — is by using platforms that combine them into a single flow. For example, with Symbiosis.finance, you can swap a token on one chain and receive a more widely accepted token on Ethereum, all in one transaction. This can save you a few steps and reduce the chance of user error when hopping between tools.

How to sell crypto with MetaMask

The simplest way to sell crypto that you hold on MetaMask is by using the application itself. Here’s what to do:

-

Open MetaMask portfolio: In your MetaMask extension or app, click the “Buy & Sell” button. This will take you to the MetaMask Portfolio site, where you can manage all your assets and begin the selling process.

-

Start the sale process: Click on “Move crypto” at the top of the page and select “Sell” from the dropdown options.

-

Choose your region and currency: MetaMask will ask for your country of residence and preferred fiat currency. This step ensures you’re shown accurate provider options and payout methods available in your area.

-

Enter sale amount: Select Ether and enter how much you’d like to convert.

-

Pick a payout option: Next, choose where you want the fiat to go. Depending on your region and provider availability, you might be able to send it to a bank account, PayPal or another method.

-

Compare offers: MetaMask aggregates offers from several third-party providers (like MoonPay, Transak, Sardine, etc.), showing you real-time exchange rates, fees and estimated payout times. Take a moment to compare and pick the best option for you.

-

Complete the sale: Once you’ve chosen a provider, MetaMask will guide you through sending the crypto. You’ll confirm the transaction in your wallet, and the funds will be transferred to the provider, who handles the fiat payout.

There are two things to keep in mind when using the MetaMask application:

-

Firstly, while the application itself might not ask you for KYC, the third-party providers will. So, expect to get your documents ready for this one.

-

Secondly, MetaMask’s sell feature only supports ETH on the Ethereum mainnet. This is where the bridging will come in as was explained earlier.

Withdrawing crypto via centralized exchanges

If you’d rather cash out your crypto through a centralized exchange, Coinbase is a popular option. It’s beginner-friendly, offers fiat withdrawals, and supports a wide range of assets. Just note: You’ll need to complete KYC verification before withdrawing any fiat.

Here’s how to do it, step by step:

1. Send crypto from MetaMask to Coinbase

First things first: You’ll need to move your funds from MetaMask to Coinbase.

-

Log in to your Coinbase account and hit “Send & Receive” at the top.

-

Switch to the “Receive” tab, pick the crypto you’re sending (like ETH or USDC), and copy the wallet address Coinbase gives you.

-

Make sure the network matches — for example, if you’re sending ETH, it should be on the Ethereum (ERC-20) network.

Now open MetaMask:

-

Click “Send,” paste in that Coinbase address, and enter how much you want to transfer.

-

Double-check the network — if you send it to the wrong one, your funds could disappear.

-

Hit “Confirm,” and your crypto should show up in Coinbase after a few minutes.

2. Sell crypto for fiat on Coinbase

Once your funds land in Coinbase, it’s time to cash out.

-

Head to “Buy & Sell” at the top and switch to the “Sell” tab.

-

Choose the crypto you just received and decide how much you want to sell.

-

Pick where you want the money to go — like your linked bank account, PayPal or your Coinbase balance.

-

Review the details (including any fees), then hit “Sell.”

Did you know? When withdrawing via centralized exchanges, be cautious of minimum withdrawal amounts and any associated fees. Check these details in advance to make sure the limits and costs are acceptable to you before committing to this route.

Peer-to-peer with KYC

With peer-to-peer (P2P), you’re not selling your crypto to the exchange. Instead, you’re selling it to another user. You choose a buyer based on their offer and preferred payment method (like bank transfer, Revolut, Wise, etc.). Once they send the money to your account, you release the crypto to them. The platform holds your crypto in escrow during the process, so no one can just disappear with your funds.

With centralized exchanges, you’ll have to complete KYC before you’re able to trade in this manner.

Selling via P2P on Binance

Go to Trade > P2P.

-

Choose the coin you want to sell and browse the list of available buyers.

-

Select a deal, confirm the order, and wait for the buyer to make the payment.

-

Once the payment has arrived in your account, confirm it and release the crypto from escrow.

Did you know? Some peer-to-peer (P2P) cryptocurrency exchanges offer a “cash by mail” option, allowing users to send physical cash through postal services or couriers to settle transactions.

Cashing out of your MetaMask wallet without KYC

For those looking to convert cryptocurrency from their MetaMask wallet to fiat currency without undergoing Know Your Customer (KYC) verification, there are still a few viable paths.

Decentralized P2P platforms let you trade directly with other users, much like their centralized counterparts, though often with minimal or no KYC requirements.

-

LocalCoinSwap: A non-custodial P2P marketplace that supports a wide range of cryptocurrencies and payment methods, including cash. It offers escrow protection and emphasizes privacy.

-

Bisq: A fully decentralized exchange that supports a variety of cryptocurrencies, including Bitcoin and Monero (XMR). It runs on a peer-to-peer protocol and doesn’t require user accounts or KYC.

However, without KYC, you’re responsible for vetting the person you’re trading with. Check their reputation, review any available trade history, and always follow platform safety guidelines.

Using cryptocurrency ATMs to withdraw crypto from MetaMask

Withdrawing funds from your MetaMask wallet using cryptocurrency ATMs — often referred to as Bitcoin ATMs — is an option that allows you to convert your digital assets into cash. Here’s how you can approach this method:

-

Locate a cryptocurrency ATM: Begin by finding a cryptocurrency ATM in your vicinity. Websites like CoinATMRadar provide directories of Bitcoin ATM locations worldwide, detailing the services they offer and the cryptocurrencies they support.

-

Prepare your MetaMask wallet: Ensure that the cryptocurrency you intend to withdraw is supported by the ATM. Bitcoin ATMs predominantly support Bitcoin (BTC), so you may need to use a decentralized exchange (DEX) to swap your current tokens for BTC within your MetaMask wallet. Be mindful of transaction fees and exchange rates during this process.

-

Initiate the withdrawal process: At the ATM, select the option to withdraw cash. The machine will prompt you to specify the amount you wish to withdraw and provide a QR code representing the ATM’s wallet address.

-

Transfer funds from MetaMask: Using your MetaMask wallet, scan the QR code provided by the ATM to input the recipient address accurately. Enter the exact amount of cryptocurrency required and confirm the transaction. Be aware that network congestion can affect transaction times.

-

Collect your cash: Once the blockchain confirms the transaction, the ATM will dispense the equivalent amount in cash, minus any applicable fees. This process can take anywhere from a few minutes to longer, depending on network conditions.

When using crypto ATMs, you should expect very high fees, and while small transactions don’t usually require KYC, larger ones still might.

Are MetaMask crypto transactions taxable?

Taxes aren’t the most exciting topic, but they matter when converting crypto from a MetaMask wallet into fiat. Selling crypto, whether through MetaMask, an exchange or a P2P deal, may trigger a taxable event, and understanding the applicable rules is essential.

Selling crypto = possibly taxable

In most countries, including the US, selling crypto for fiat (like US dollars, euros, etc.) is treated like selling property. That means if you bought ETH at $1,000 and sold it later for $1,500, you’ve made a $500 capital gain — and that’s usually taxable.

Even swapping one crypto for another (say, ETH for USDC) can trigger the same kind of tax obligation, even if no fiat is involved. So, yeah, it’s not just cashing out that counts — any trade can be reportable.

To stay on top of it, keep a record of:

-

When you bought and sold each asset

-

How much you bought and/or sold

-

What it was worth in fiat at the time

-

Any fees paid along the way.

These details make life way easier when tax season rolls around — or if your accountant gives you that look.

Know your local rules

Crypto laws aren’t one-size-fits-all. Every country has its own stance, and even within the same country, rules can vary depending on how you’re using crypto.

In the US, for example, selling crypto could fall under capital gains tax rules or even money transmission laws, depending on how you’re moving the funds. Other countries might have more lenient — or much stricter — regulations.

So, here’s what to do:

-

Look up your local crypto tax laws (even if they seem vague or outdated).

-

Stay current — regulations are evolving fast.

-

Talk to a pro if you’re unsure. A crypto-savvy accountant or legal adviser can help you avoid nasty surprises.

Even if you’re using non-KYC methods or decentralized tools, tax authorities may still expect a full report. Being proactive about it will save you headaches later — and might even save you money.

Happy cashing out!

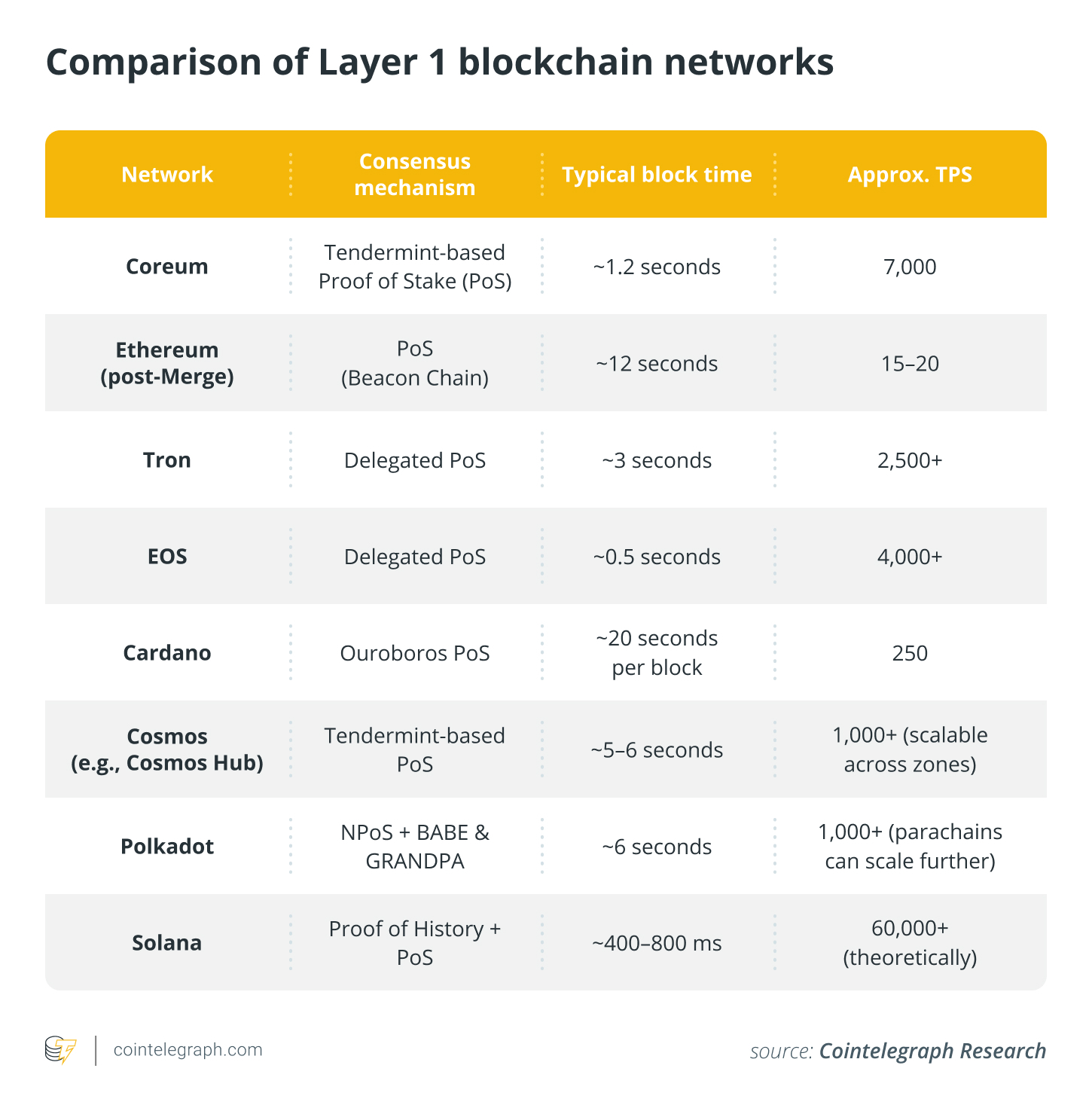

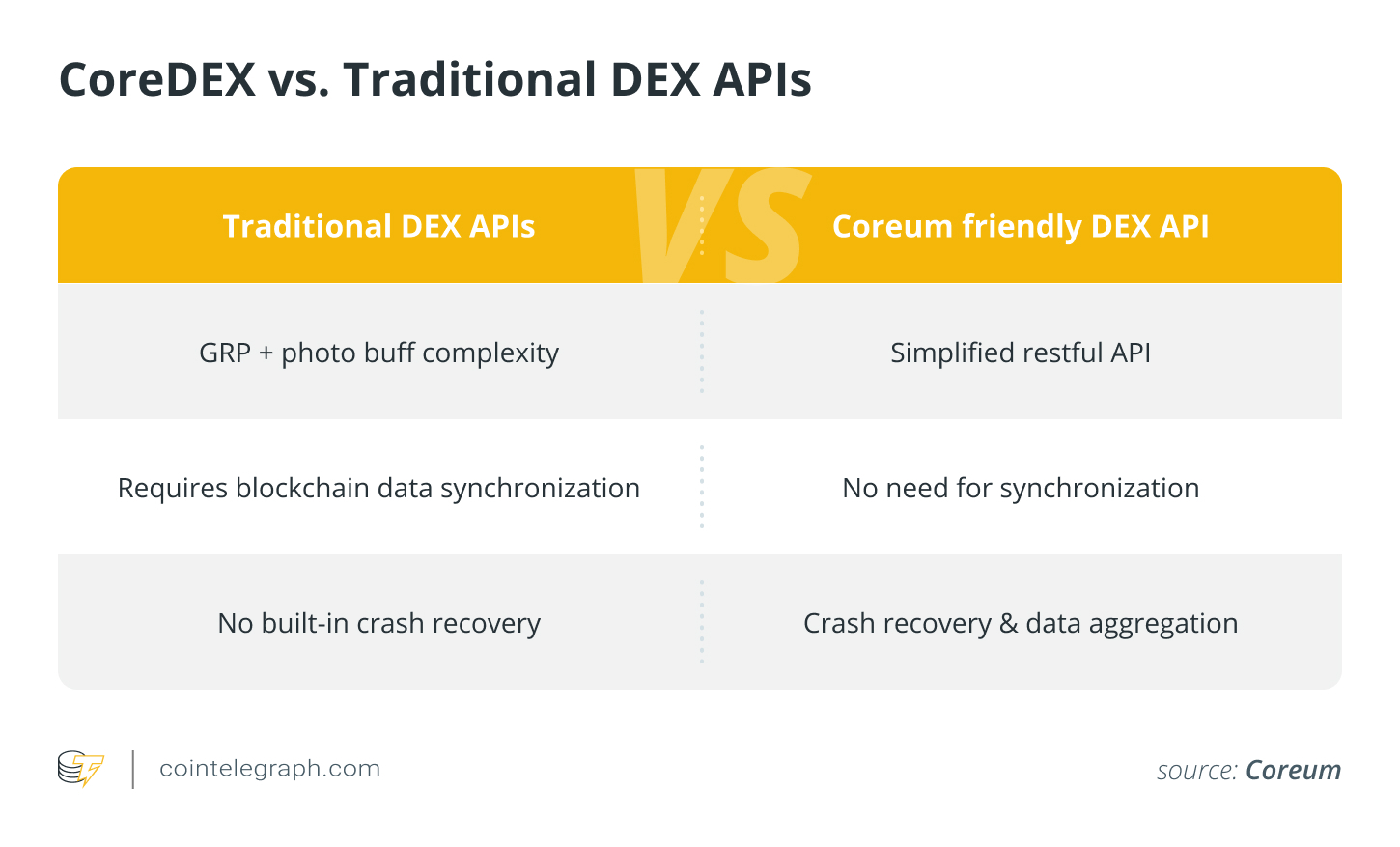

Coreum: How a 7,000 TPS blockchain is shaping the future of regulated finance

A new report by Cointelegraph Research explores Coreum’s role in institutional blockchain adoption. It analyzes the project’s technical architecture, compliance framework and its potential impact on regulated asset tokenization. The report presents insights into transaction efficiency, security mechanisms and crosschain interoperability. It also evaluates how […]

Analysis

A new report by Cointelegraph Research explores Coreum’s role in institutional blockchain adoption. It analyzes the project’s technical architecture, compliance framework and its potential impact on regulated asset tokenization. The report presents insights into transaction efficiency, security mechanisms and crosschain interoperability. It also evaluates how Coreum fits into the evolving financial landscape.

Blockchain evolution and institutional requirements

The adoption of blockchain technology by financial institutions has been increasing in lockstep, with the value locked in tokenized real-world assets (RWA). The latter grew by 85% in 2024.

Our report examines how third-generation blockchains, such as Coreum, are addressing the challenges of scalability, regulatory compliance and interoperability. Improvements in the infrastructure on the base layer will lead to more seamless institutional adoption in the future.

Read the full version of the report for free here.

Coreum is structured to support applications that require predictable transaction costs, regulatory oversight and seamless integration with financial infrastructure. Network data indicates that Coreum achieves a transaction throughput in excess of 7,000 TPS and a time to finality of about 1.2 seconds. This positions Coreum well in a crowded and highly competitive layer-1 blockchain landscape.

Coreum integrates most of its compliance features at the protocol level, a critical factor for institutional adoption. The network includes onchain KYC and AML monitoring in collaboration with AnChain.ai, an AI-driven compliance provider.

This is unlike conventional blockchains, where compliance tools are third-party application-layer software. Coreum puts compliance at its foundation together with real-time risk assessment and fraud detection.

Decentralized exchange (DEX) and institutional trading infrastructure

Our report also analyses Coreum’s decentralized exchange (DEX) infrastructure. While many layer-1 blockchains rely on liquidity pools, Coreum features a built-in onchain order book. There are important differences between the models.

Coreum’s order book DEX allows for deterministic trade execution with minimal slippage, which makes it well-suited for institutional trading strategies. In contrast, AMM-based DEXs rely on liquidity pools that sometimes lead to price inefficiencies and higher exposure to impermanent loss.

Coreum’s DEX architecture also supports high-frequency trading, with transaction processing speeds comparable to traditional financial exchanges.

A notable aspect of Coreum’s DEX is its advanced API, which enables integration with institutional trading systems. The API is designed to provide low-latency access to order book data, market execution tools and automated trading strategies.

This infrastructure allows financial firms and market makers to integrate Coreum’s DEX into their existing trading workflows. It ensures compliance with industry standards and benefits from blockchain-based settlement efficiencies.

Read the full version of the report for free here.

Interoperability and network connectivity

Coreum’s interoperability strategy includes connections with the XRP Ledger (XRPL) and the Cosmos/IBC network. These integrations enable crosschain liquidity and asset transfers, which creates support for financial applications that require seamless movement between blockchain ecosystems.

This integration allows institutional users to leverage XRPL’s efficiency in payments and Cosmos’ modular interoperability framework with over 100 connected chains. The ability to interact with multiple networks without sacrificing security or compliance aligns with institutional requirements for blockchain adoption.

The Future of Regulated Blockchain Infrastructure:

Networks designed for institutional adoption will need to address compliance, scalability and interoperability challenges. Coreum’s technical structure and regulatory considerations provide a case study for how blockchain networks may evolve to meet these requirements.

With its deterministic fee structure, built-in compliance framework and high-speed trading infrastructure, Coreum represents an example of how third-generation blockchains are positioning themselves at the intersection of crypto and regulated financial markets.

Read the full version of the report for free here

Disclaimer. This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.

This article is for general information purposes and is not intended to be and should not be taken as legal or investment advice. The views, thoughts, and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Cointelegraph does not endorse the content of this article nor any product mentioned herein. Readers should do their own research before taking any action related to any product or company mentioned and carry full responsibility for their decisions.

Smart money concepts in crypto trading: How to track and profit

Key takeaways Smart money consists of institutional investors with advanced tools and knowledge that can influence crypto market trends. Key concepts like order blocks, liquidity zones and fair value gaps can help traders align with smart money strategies. Real-time tracking tools such as Glassnode, Nansen […]

Analysis

Key takeaways

-

Smart money consists of institutional investors with advanced tools and knowledge that can influence crypto market trends.

-

Key concepts like order blocks, liquidity zones and fair value gaps can help traders align with smart money strategies.

-

Real-time tracking tools such as Glassnode, Nansen and CoinGecko allow traders to follow smart money’s moves and capitalize on them.

-

Following the movements of smart money is akin to navigating the open sea, using its wake to position yourself for success in the crypto market.

Smart money consists of institutional investors with advanced tools and knowledge that can influence crypto market trends.

Key concepts like order blocks, liquidity zones and fair value gaps can help traders align with smart money strategies.

Real-time tracking tools such as Glassnode, Nansen and CoinGecko allow traders to follow smart money’s moves and capitalize on them.

Following the movements of smart money is akin to navigating the open sea, using its wake to position yourself for success in the crypto market.

Smart money refers to the money being invested by individuals or organizations that know the markets inside and out. We’re talking about institutional investors, hedge funds and well-seasoned traders. These are the big players who have access to more information and tools than most of us, and they use that knowledge to make strategic decisions.

In the crypto world, “smart money” is especially powerful because the market is still growing and changing quickly. These investors have a massive impact on the market. Their moves can shake things up, push prices up or down and even shift the way people feel about a particular coin or token.

For example, when major players like BlackRock launch a Bitcoin exchange-traded fund (ETF), it can send waves through the market, influencing Bitcoin’s (BTC) price and the broader market.

How do institutional investors influence crypto market trends?

Institutional investors have substantial financial muscle, and when they enter the crypto market, they can make a big impact in several ways:

-

Liquidity and stability: These investors bring in large amounts of capital, which makes it easier to buy and sell without dramatically affecting prices. This helps stabilize the market and makes it more attractive for other investors to get involved. When more money is flowing in and out smoothly, it creates a healthier, more balanced market.

-

Price movements and volatility: When these big players make large investments (or sell off their holdings), it can cause prices to move quickly, either up or down. While this can create volatility, it also opens the door for traders to take advantage of those price swings.

-

Regulation and legitimacy: As institutional investors get involved, they push for clearer regulations, which helps bring more legitimacy to the crypto space. For instance, the approval of Bitcoin ETFs has given institutional investors a regulated way to invest in Bitcoin, and that’s made the market more credible overall.

In short, smart money is invested by experienced, informed players who make strategic moves, while ordinary money is often invested by individuals without deep market knowledge or insight.

Smart money concepts (SMC) in crypto trading

SMC is a trading strategy focused on analyzing and capitalizing on the movements of smart money. The key elements of SMC include order blocks, liquidity zones and fair value gaps. Let’s break these down simply.

Order blocks (OB)

Order blocks are areas on the chart where big investors (the smart money) are making large buy or sell orders. These areas usually act like walls of support or resistance, meaning they are strong levels where prices tend to bounce back. You can spot order blocks by looking for clusters of high-volume candlesticks at certain price levels. These are often periods of sideways price movement followed by a sharp move up or down.

When the price comes back to these areas, expect it to react in some way, as that’s where the smart money has been.

Liquidity zones

Liquidity zones are collections of buy and sell orders at certain price points. These are like gathering spots where a lot of market participants are placing their orders, creating areas where price reversals or breakouts are likely to happen.

Smart money investors love these zones because they can place large trades without drastically moving the market in one direction or the other. By understanding where liquidity zones are, you can predict where the market might go next.

Fair value gaps (FVG)

A fair value gap occurs when there’s a big imbalance between the buy and sell orders for an asset, creating a gap on the chart. This usually happens when the price moves quickly without much trading in between, and you can spot these gaps as spaces between candlesticks.

These gaps act like magnets for the price. Markets often return to fill these gaps before continuing their trend. When you spot a gap, it could be a great opportunity to enter the market, knowing the price might come back to fill it before resuming its movement.

How to track smart money moves in real time

There are several tools that help decode blockchain data and spot smart money maneuvers instantly.

1. Glassnode

Category: On-chain analytics

Website: glassnode.com

Glassnode gives you visibility into blockchain data unavailable through price charts alone. It shows how crypto flows between wallets, exchanges, and large holders, which is perfect for tracking institutional activity.

Key features for smart money tracking:

-

Exchange inflows/outflows: Watch for sudden spikes in BTC or Ether (ETH) moving in/out of exchanges, often a sign that big players are preparing to buy or sell.

-

Whale metrics: Metrics like “Number of addresses holding 10K+ BTC” help identify when whales are accumulating or distributing.

-

Realized cap and dormancy: This tells you whether older coins are moving, often a clue that long-term holders (smart money) are repositioning.

Top tip! If you notice a sharp drop in exchange reserves for ETH on Glassnode, that could signal whales are withdrawing ETH to cold storage (a bullish sign). Combine this with price action, and you may have a high-confidence entry point.

2. Nansen

Category: Wallet and whale tracking

Website: nansen.ai

Key features for smart money tracking:

-

Smart money dashboard: A curated list of wallets considered “smart” based on their historical returns and behavior.

-

Token god mode: See what tokens smart money is buying or selling and how holdings have changed over time.

-

Real-time alerts: Set alerts for transactions by specific wallets or token movements.

Top tip! Suppose that you see that multiple smart money wallets started buying a low-cap altcoin over the past 24 hours. That might be a sign they know something before the broader market does. You can monitor for a breakout and act accordingly.

3. CoinGecko

Category: Market data and volume analysis

Website: coingecko.com

Key features for smart money tracking:

-

Volume spikes: Watch for sudden increases in 24-hour volume that are not yet reflected in price — often a prelude to a move.

-

Liquidity data: Find coins with deep liquidity where institutions might be operating.

-

Exchange data: Monitor volume by exchange. If one exchange suddenly has massive buy pressure, smart money might be active there.

Top tip! Perhaps a small-cap token sees a 5x spike in volume on Binance but hasn’t moved much in price yet. That divergence can indicate accumulation. You could do a deeper dive with onchain tools Nansen or Glassnode to confirm.

4. Santiment

Category: Market sentiment and onchain analytics

Website: santiment.net

Key features for smart money tracking:

-

Social volume and sentiment: Gauge hype levels around tokens. Smart money often moves counter to the crowd.

-

Whale transaction count: See how many large transactions (e.g., $100,000+) are happening for a given coin.

-

Development activity: Some smart money tracks developer activity as a proxy for long-term value.

Top tip! A token sees decreasing positive sentiment but a spike in whale transactions. That disconnect can signal smart money is accumulating while retail exits, a classic contrarian play.

5. Chainalysis

Category: Blockchain forensics and risk detection

Website: chainalysis.com

Chainalysis focuses more on risk detection and compliance, but it can still be useful to track large, high-risk wallet movements and avoid traps or manipulated markets.

Key features for smart money tracking:

-

Address labeling: Know whether a wallet belongs to an exchange, scam, hacker group or institutional custodian.

-

Transaction monitoring: Track big inflows/outflows and the origin of funds. Are they from DeFi protocols, over-the-counter (OTC) desks or mixers?

-

Risk scoring: Avoid getting caught in tokens or wallets associated with pump-and-dump schemes or hacks.

Top tip! If you see a large amount of ETH being sent from a wallet flagged as a known DeFi VC to an exchange, that could be a sign of upcoming selling pressure. Conversely, tracking inflows to cold wallets from institutions can be a bullish signal.

Follow the Man o’ War

Think of crypto trading as the open sea, with smart money as powerful Man o’ War ships, navigating with advanced tools and knowledge. As a retail trader, you may not be in control of these ships, but you can follow their course.

Using platforms such as Glassnode, Nansen, CoinGecko, Santiment and Chainalysis, you can track the movements of smart money in real-time. While you might not steer the ship, by observing its wake, you can adjust your course and position yourself for profitable opportunities.

You don’t need to command the ship; just follow its lead to find your way to safe, profitable shores.

How to file crypto taxes in the US (2024–2025 tax season)

Key takeaways US crypto investors must file their 2024 tax returns by April 15, 2025, ensuring all crypto transactions are accurately reported to the IRS. Crypto held for less than a year is taxed as ordinary income (10%-37%), while holdings over a year qualify for […]

Analysis

Key takeaways

-

US crypto investors must file their 2024 tax returns by April 15, 2025, ensuring all crypto transactions are accurately reported to the IRS.

-

Crypto held for less than a year is taxed as ordinary income (10%-37%), while holdings over a year qualify for lower capital gains rates (0%, 15%, or 20%).

-

Selling, trading, or spending crypto triggers taxes, while holding or transferring between wallets does not.

-

Mining, staking, airdrops, and crypto payments are taxed as income at applicable rates.

US crypto investors must file their 2024 tax returns by April 15, 2025, ensuring all crypto transactions are accurately reported to the IRS.

Crypto held for less than a year is taxed as ordinary income (10%-37%), while holdings over a year qualify for lower capital gains rates (0%, 15%, or 20%).

Selling, trading, or spending crypto triggers taxes, while holding or transferring between wallets does not.

Mining, staking, airdrops, and crypto payments are taxed as income at applicable rates.

The world of cryptocurrencies can indeed be an exciting space for investors, but as the tax season approaches, many US investors find themselves grappling with confusion and uncertainty.

With the upcoming tax filing deadline of April 15, 2025, it’s a critical time to get a handle on crypto tax obligations. Ask most US crypto investors, and they’ll likely tell you that figuring out what transactions trigger a taxable event feels like navigating a maze.

Understanding various aspects of tax filing is crucial for accurately filing taxes, avoiding penalties and staying compliant with the Internal Revenue Service (IRS). This article breaks down key elements like tax brackets, rates, exemptions and other critical details.

How does the IRS tax crypto?

The Internal Revenue Service, the agency responsible for collecting US federal taxes, treats cryptocurrencies as property for tax purposes. You pay taxes on gains realized when selling, trading or disposing of cryptocurrencies. For short-term capital gains (held less than a year), you pay taxes at the rates of 10%–37%, depending on your income bracket.

Long-term capital gains (assets held for over a year) benefit from reduced rates of 0%, 15% or 20%, also based on your taxable income.

When you dispose of cryptocurrency for more than its purchase price, you generate a capital gain. Conversely, selling below the purchase price results in a capital loss. You must report both your capital gains and losses for the year in which the transaction occurs, with gains being taxable and losses potentially offsetting gains to reduce your tax liability.

With the upcoming April 15, 2025, deadline for filing 2024 tax returns, US crypto investors need to ensure these transactions are accurately tracked and reported.

To illustrate, suppose you purchased Ether (ETH) worth $1,000 in 2023 and sold it after a year in 2024 for $1,200, netting a $200 profit. The IRS would tax that $200 as a long-term capital gain, applying the appropriate rate based on your 2024 income.

Taxes are categorized as capital gains tax or income tax, depending on the type of transactions:

-

Capital gains tax: Applies to selling crypto, using crypto to purchase goods or services, or trading one cryptocurrency for another.

-

Income tax: Applies to crypto earned through mining, staking, receiving it as payment for work, or referral bonuses from exchanges.

These distinctions are crucial for accurate reporting by the April 15 deadline. Gains are taxed, while losses can help offset taxable income, so detailed record-keeping is a must.

Did you know? In Australia, gifting cryptocurrency triggers a capital gains tax (CGT) event. The giver may need to report gains or losses based on the asset’s market value at the time of transfer, though certain gifts — like those between spouses — may qualify for exemptions. While this differs from US rules, it highlights how crypto taxation varies globally.

How crypto tax rates work in the US

In the US, your crypto tax rate depends on your income and how long you’ve held the cryptocurrency. Long-term capital gains tax rates range from 0% to 20%, and short-term rates align with ordinary income tax rates of 10%–37%. Transferring crypto between your own wallets or selling it at a loss doesn’t trigger a tax liability.

You only owe taxes when you sell your crypto, whether for cash or for any other cryptocurrency. Consider this example: Suppose you bought crypto for $1,000 in 2024, and by 2025, its value rose to $2,000. If you don’t sell, no tax is due — unrealized gains aren’t taxable.

If you sell cryptocurrency after holding it for a year or less, your profits are subject to short-term capital gains tax. These gains are taxed as ordinary income, meaning they are added to your total taxable earnings for the year.

Tax rates are progressive, based on income brackets, so different portions of your income are taxed at different rates. For instance, a single filer in 2025 pays 10% on the first $11,000 of taxable income and 12% on income up to $44,725. Short-term rates are higher than long-term rates, so timing your sales can significantly impact your tax bill.

Understanding crypto capital gains tax in the US

If you sell cryptocurrency after holding it for a year or less, your profits are subject to short-term capital gains tax. These gains are treated as ordinary income and added to your total taxable earnings for the year. Since tax rates are based on income brackets, different portions of your earnings are taxed at different rates, as explained above.

2024–2025 federal income tax brackets for crypto earnings

Here are the federal income tax rates for the 2024–2025 tax year. You apply the 2024 tax brackets to income earned in the 2024 calendar year, reported on tax returns filed in 2025.

Long-term capital gains tax for crypto earned in 2024

You pay long-term capital gains tax if you sell cryptocurrency after holding it for more than a year. Unlike short-term gains, these aren’t taxed as ordinary income. Instead, tax rates are based on your total taxable income and filing status. Long-term capital gains tax rates are 0%, 15% or 20%, making them lower than short-term rates. Holding crypto longer can reduce your tax burden significantly.

Here is a table outlining long-term crypto capital gains tax for the calendar year 2024. These rates are applicable when filing tax returns in 2025.

2024–2025 standard deduction: Reduce your crypto taxable income

The standard deduction is the portion of your income that’s exempt from federal taxes before tax rates are applied, reducing your taxable income.

Here is a table regarding tax deductions in the calendar year 2024. These amounts are applicable when filing for tax returns in 2025.

How are crypto airdrops taxed in the US?

In the US, crypto airdrops are treated as ordinary income by the IRS and taxed at the time they come under the taxpayer’s full control. The taxable amount is based on the tokens’ fair market value at that moment, even if the taxpayer didn’t request them. Later, selling or trading those tokens may trigger capital gains tax, depending on the price difference between receipt and disposal.

The taxable event hinges on control: If tokens automatically appear in a taxpayer’s wallet, the income is typically recognized upon arrival. If the tokens require manual claiming (e.g., through a transaction), the taxable event occurs when the claim is completed. Either way, the fair market value at that point determines the income reported.

When the taxpayer sells or trades the airdropped tokens, they incur a capital gain or loss, calculated as the difference between the value at receipt (the basis) and the value at sale or trade. Moreover, the holding periods matter: If sold within a year, gains are taxed at ordinary income rates (10%–37%, based on income brackets). If held longer than a year, gains qualify for lower long-term capital gains rates (0%, 15% or 20%, depending on income). Proper tracking of receipt dates and values is essential for accurate tax reporting.

Crypto gifting rules and tax implications in the US

In the US, gifting cryptocurrency is generally not a taxable event for either the giver or the recipient, meaning no immediate tax is owed. However, specific thresholds and reporting requirements must be followed to stay compliant with IRS rules.

For the 2024 tax year (filed by April 15, 2025), if the total value of crypto gifts to a single recipient exceeds $18,000, the giver must file a gift tax return using Form 709.

When the recipient eventually sells the gifted cryptocurrency, they’ll calculate capital gains or losses based on the giver’s original cost basis — the price the giver paid for the crypto. If this cost basis isn’t documented or available, the recipient may need to assume a basis of $0, which could increase their taxable gain upon sale. To avoid complications, both parties should keep detailed records of the gift’s fair market value at the time of transfer and the giver’s original cost basis.

Did you know? In the UK, giving cryptocurrency as a gift may result in capital gains tax for the giver, except for gifts to spouses or civil partners. Additionally, inheritance tax could apply if the giver dies within seven years of the gift.

Essential forms for filing crypto taxes in 2024

With the April 15, 2025, deadline nearing, here are the key forms for reporting 2024 crypto transactions:

-

Form 8949: For reporting capital gains and losses from crypto sales, trades and disposals. Each transaction must be listed individually.

-

Schedule D (Form 1040): Summarizes total capital gains and losses from Form 8949; used for calculating taxable income.

-

Schedule 1 (Form 1040): Reports additional income, including staking rewards, airdrops and hard forks, if classified as taxable income.

-

Schedule C (Form 1040): Used by self-employed individuals or businesses to report crypto-related income from mining, consulting or freelance work.

-

Form 1099-MISC: Issued for staking, mining or payment income over $600

-

Form 1040: The main return form to combine income, deductions and tax liability.

-

FBAR (FinCEN Form 114): File separately if foreign crypto accounts exceeded $10,000 in 2024.

Step-by-step guide to filing crypto taxes for the 2024–2025 tax season

Here’s how to file, step by step, leveraging the detailed tax rates and forms outlined above.

Step 1: Gather all crypto transaction records

Collect records for every 2024 crypto transaction:

-

Dates of buying, selling, trading or receiving crypto

-

Amounts (e.g., 0.5 Bitcoin) and US dollar fair market value (FMV) at the time

-

Cost basis (what you paid, including fees) and proceeds (what you received).

To ensure complete records, pull data from wallets, exchanges (e.g., Coinbase) and blockchain explorers. Export transaction histories or CSVs, and note staking rewards, airdrops or mining income separately with their FMV on receipt.

Step 2: Identify taxable events

Pinpoint which 2024 actions trigger taxes:

-

Taxable: Selling crypto for cash/stablecoins, trading crypto, spending crypto or earning it (mining, staking, airdrops).

-

Non-taxable: Buying and holding with USD, moving crypto between your wallets, gifting up to $18,000 per recipient.

Classify each taxable event as short-term (≤1 year) or long-term (>1 year) for rate purposes.

Step 3: Calculate capital gains and losses

For taxable sales or trades:

-

Formula: Proceeds (FMV at disposal) – Cost Basis = Gain/Loss

-

Example: Bought 1 Ether (ETH) for $2,000 in May 2024, sold for $2,500 in November 2024 = $500 short-term gain.

Use first-in, first-out or specific identification for cost basis (be consistent). Sum your net gains/losses. See the “2024 Federal Income Tax Brackets” section for how these are taxed.

Step 4: Calculate crypto income

For earnings (mining, staking, airdrops):

-

Record FMV in USD when received (e.g., 10 Cardano worth $5 on June 1, 2024 = $5 income).

-

Add to your other 2024 income to set your tax bracket, detailed in the sections above.

Step 5: Apply the 2024 standard deduction

Lower your taxable income with the standard deduction:

-

Single: $14,600

-

Married filing jointly: $29,200

-

Head of household: $21,900

Subtract this from total income (including short-term gains and crypto income). Long-term gains are taxed separately.

Step 6: Determine your tax rates

Apply rates to your gains and income (refer to “How Crypto Tax Rates Work in 2024”):

-

Short-term gains and income: Ordinary rates (10%–37%).

-

Long-term gains: 0%, 15% or 20%, based on income.

-

Offset gains with losses (up to $3,000 net loss against other income; carry forward excess).

Step 7: Complete the necessary tax forms

Fill out the required IRS forms (see “Essential Forms for Filing Crypto Taxes in 2024”):

-

List capital gains/losses and income on Form 8949, Schedule D and Schedule 1 as applicable.

-

Use Schedule C if self-employed (e.g., mining business).

-

Combine everything on Form 1040.

-

Check Form 1099-MISC if received and file FBAR for foreign accounts over $10,000.

Step 8: File your return by April 15, 2025

-

Submit via IRS e-file or mail, postmarked by April 15, 2025.

-

Need more time? File Form 4868 for an extension to Oct. 15, 2025, but pay estimated taxes by April 15 to avoid penalties.

Step 9: Pay any taxes owed

Estimate your tax from Step 6, then pay via IRS Direct Pay or check. Late payments after April 15 incur a 0.5% monthly penalty plus interest.

Step 10: Keep records for audits

Store transaction records and forms for three to six years. The IRS is intensifying crypto scrutiny — be prepared.

Did you know? In Canada, giving cryptocurrency as a gift is generally considered a taxable disposition, requiring the giver to determine and report any capital gains or losses.

Important dates and deadlines for 2024–2025 tax season and beyond

Here are important dates regarding the 2024–2025 tax season and 2025 transition:

2024 tax season

-

Jan. 31, 2025: Some exchanges may issue voluntary 1099s (e.g., 1099-MISC).

-

April 15, 2025: File taxes on crypto earned in 2024.

2025 transition

-

Jan. 1, 2025: Form 1099-DA reporting begins.

-

Dec. 31, 2025: Safe harbor ends for adjusting universal cost basis.

-

Jan. 31, 2026: Receive Form 1099-DA for 2025 trades.

Quarterly estimates

-

June 15, Sept. 15, 2025, etc., for active traders.

New IRS crypto tax rules for 2025: What you need to know

The IRS introduced new rules for tax filing and reporting aimed at US cryptocurrency taxpayers, but these regulations have encountered significant pushback. Both the US Senate and House of Representatives voted to repeal them under the Congressional Review Act (CRA), and President Donald Trump has signaled support for the rollback. Despite this uncertainty, understanding these rules remains crucial, especially with deadlines looming in 2025.

A core component of the new rules is calculating taxes using a cost basis — the original amount invested in an asset, including fees or commissions. Accurately tracking cost basis is vital for proper tax reporting and prevents double taxation on reinvested earnings. It’s the starting point for determining capital gains or losses.

Under the updated IRS guidelines, crypto investors must now track the cost basis (original purchase price) separately for each account or wallet, moving away from a universal tracking approach. This requires recording the purchase date, acquisition cost and specific transaction details.

The rules also mandate specific identification for every digital asset sale, requiring taxpayers to report the exact purchase date, quantity and cost of the assets sold. If this information isn’t provided, the IRS defaults to the first-in, first-out (FIFO) method — selling your earliest coins first — which could inflate taxable gains if those initial purchases had lower costs.

For taxpayers previously using a universal cost basis method, the IRS requires reallocating their basis across all accounts or wallets accurately by Dec. 31, 2025, to comply with these standards.

Form 1099-DA: What to expect for crypto taxes in 2025–2026

As of March 27, 2025, Form 1099-DA is set to become a pivotal tool for the 2025–2026 tax season, simplifying how cryptocurrency transactions are reported in the US. This new form, tailored specifically for digital assets, will be issued by exchanges to both taxpayers and the IRS, providing a detailed breakdown of activities like sales, trades and other taxable crypto events from 2025.

It’s designed to streamline compliance and bolster IRS oversight, reflecting the agency’s growing focus on tracking digital asset income. For taxpayers, it promises easier, more accurate reporting, while exchanges take on a larger role in tax documentation.

For the 2024 tax year — due by April 15, 2025 — this form isn’t yet available; filers must still rely on existing forms like Form 1099-MISC until Form 1099-DA officially takes effect for 2025 earnings.

IRS crypto tax penalties: What happens if you don’t report or under-report in 2024?

US taxpayers who fail to meet their tax obligations may face penalties from the IRS. When tax obligations go unmet, the IRS sends a notice or letter detailing the penalty, its reason (e.g., late filing, non-payment or inaccurate reporting) and your next steps.

Penalties vary:

-

Late filing or non-payment can incur fines up to 25% of the unpaid tax, plus interest that accrues until settled.

-

Other triggers — like bounced checks or fraudulent claims — add further costs, and the IRS may launch an audit to scrutinize your filings.

-

Individuals may face penalties of up to $100,000 and criminal sanctions, including imprisonment for up to five years.

-

Corporations can be fined up to $500,000.

These stakes are high, especially as the IRS ramps up crypto enforcement in 2024. To dodge these consequences, double-check any notice for accuracy and act fast: Request a filing extension with Form 4868 if needed (due by April 15, 2025), arrange a payment plan for unaffordable penalties, or dispute the penalty if you believe it’s unjustified. Prompt action can save you from escalating costs and legal headaches.

Is Cardano (ADA) a “zombie crypto”?

For years, Cardano (ADA) has been a cornerstone of the crypto landscape, consistently ranking among the top digital assets by market capitalization. Yet, despite its prominence, ADA’s performance has left many investors questioning its long-term prospects. While it recently made headlines for being included in […]

Analysis

For years, Cardano (ADA) has been a cornerstone of the crypto landscape, consistently ranking among the top digital assets by market capitalization. Yet, despite its prominence, ADA’s performance has left many investors questioning its long-term prospects.

While it recently made headlines for being included in US President Donald Trump’s initial proposal for a national crypto stockpile, its price action and onchain activity tell a different story — one that has even led some critics to brand it a “zombie.”

Recent findings suggest that the ecosystem behind ADA, the Cardano network, lags significantly behind in decentralized finance (DeFi) adoption. With only a fraction of the total value locked (TVL) compared with Ethereum and Solana, Cardano struggles to attract liquidity and stablecoin activity.

While some argue that its DeFi sector is still in its early stages, several newer blockchains have outpaced it in user engagement and trading volume. The question now is whether upcoming developments can reverse the trend.

With key catalysts on the horizon, such as a potential ADA exchange-traded fund (ETF) and its emerging role in Bitcoin’s DeFi ecosystem, 2025 could be a pivotal year for ADA. But will these developments be enough to turn the tide?

To uncover the full story and explore the current state of Cardano’s native token, watch the full video now on the Cointelegraph YouTube channel!

How to buy Bitcoin in Australia

Key takeaways Bitcoin is legal in Australia and is regulated by AUSTRAC and the Australian Taxation Office (ATO). You can buy Bitcoin on various platforms, including centralized exchanges, decentralized exchanges (DEXs), P2P platforms and Bitcoin ATMs Payment options are diverse, including credit cards, debit cards, […]

Analysis

Key takeaways

-

Bitcoin is legal in Australia and is regulated by AUSTRAC and the Australian Taxation Office (ATO).

-

You can buy Bitcoin on various platforms, including centralized exchanges, decentralized exchanges (DEXs), P2P platforms and Bitcoin ATMs

-

Payment options are diverse, including credit cards, debit cards, bank transfers and fiat cash deposits at ATMs

-

Store your Bitcoin securely and opt for cold wallets, which protect you better than custodial wallets from crypto exchanges.

Bitcoin is legal in Australia and is regulated by AUSTRAC and the Australian Taxation Office (ATO).

You can buy Bitcoin on various platforms, including centralized exchanges, decentralized exchanges (DEXs), P2P platforms and Bitcoin ATMs

Payment options are diverse, including credit cards, debit cards, bank transfers and fiat cash deposits at ATMs

Store your Bitcoin securely and opt for cold wallets, which protect you better than custodial wallets from crypto exchanges.

Bitcoin adoption continues to grow. More and more Australians are discovering the cryptocurrency as an investment vehicle, with ownership rising from 23% in 2023 to 32.5% in 2025, an impressive 41.3% increase. Because there are several platforms to choose from, buying Bitcoin is low-threshold and secure.

This article covers several methods and describes the steps to safely start investing in Bitcoin.

Is Bitcoin legal in Australia?

Yes, Bitcoin is legal in Australia, but it’s not considered a legal tender. The local government considers owning cryptocurrencies like Bitcoin (BTC) as property. Any profit you might make from Bitcoin is subject to capital gains tax (CGT), with Australian Transaction Reports and Analysis Centre (AUSTRAC) ensuring AML and CTF compliance.

Of course, there are also various regulatory requirements to abide by. AUSTRAC requires cryptocurrency companies to comply with Anti-Money Laundering (AML) and counter-terrorism-financing (CTF) regulations. This framework aims to protect Australian investors by safeguarding the crypto market against financial crime.

A significant update in 2025 requires major crypto platforms to obtain an Australian Financial Services License (AFSL) for enhanced consumer protection, as outlined in government proposals.

Did you know? Some Australian exchanges offer instant verification, allowing you to start trading Bitcoin within minutes.

Prerequisites to buying Bitcoin in Australia

Before buying Bitcoin in Australia, it is essential to prepare properly. To get you started, here are some points of interest:

-

Understand the legal landscape: Bitcoin is legal and regulated in Australia by AUSTRAC, but it is not a legal tender. You can safely deal with cryptocurrencies because the government minimizes risks such as money laundering.

-

Platforms to buy Bitcoin in Australia: If you want to buy Bitcoin or other crypto assets in Australia, use a reliable platform. Choose CoinSpot, Swyftx or Binance. These exchanges comply with local regulations, allowing you to trade safely. Of course, don’t forget to complete your KYC verification. Please note that Binance offers spot trading only, as its derivatives license was canceled in 2023.

-

Set up a non-custodial wallet for self-custody: Choose a non-custodial wallet, such as Trust Wallet or Exodus. This allows you to keep control of your private keys. If you go for long-term storage of your coins, always choose a cold wallet that stores your assets offline.

-

Payment methods and fees: The fastest and safest way is to initiate transactions with a reliable payment method, such as bank transfer, credit card or PayID. Always check the associated transaction fees so you don’t incur unexpected (sometimes high) fees.

-

Secure your investment: Take precautions for your security, too. Enable two-factor authentication (2FA) on your accounts and back up private keys regularly. Ensure your platform offers strong security features such as encryption and cold storage.

How to buy Bitcoin in Australia on a centralized exchange

Want to buy Bitcoin through a central exchange, such as CoinSpot? You can do this easily and quickly:

-

Step 1: Create an account. Sign up to CoinSpot with your email address and a secure password. Go through the KYC process with ID verification and get started. As of 2025, CoinSpot complies with AUSTRAC regulations and the new AFSL requirement, ensuring enhanced consumer protection.

-

Step 2: Add a payment method. Link a payment method, such as bank transfer, debit card or Australian-only PayID. CoinSpot supports low-fee options like bank transfers (free via POLi) and PayID, while credit/debit card transactions may incur fees up to 2.58%, so review these costs upfront.

-

Step 3: Navigate to the Bitcoin purchase section. Go to “Buy/Sell” on CoinSpot’s website or in the app and select Bitcoin from the list of over 350 supported cryptocurrencies.

-

Step 4: Enter the amount. Enter how much Bitcoin you want to buy in AUD. The platform will display how much Bitcoin you are buying based on the current exchange rate.

-

Step 5: Check the transaction. Check the details, including fees, before confirming the purchase.

-

Step 6: Confirm and complete the purchase. Click “Buy Now” to complete the transaction. The Bitcoin you bought will appear immediately in your CoinSpot wallet. For added security, you could consider transferring your BTC to a non-custodial wallet like Exodus after purchase to retain full control over your private keys.

This efficient process makes Bitcoin accessible to beginners and experienced users, all in a secure, regulated environment.

How to buy Bitcoin in Australia using a non-custodial wallet

Non-custodial wallets give you full control over your Bitcoin. If you want to know how to buy Bitcoin with your Trust Wallet, go through the steps below:

-

Step 1: Set up a Trust Wallet. Download Trust Wallet from the App Store or Google Play. Create a wallet, set a secure password and write down the 12-word recovery phrase.

-

Step 2: Link a payment method. Link a payment method, such as a debit card or bank transfer, via MoonPay or Simplex. Use a service that supports Trust Wallet in Australia.

-

Step 3: Select Bitcoin and start the purchase. Tap “Buy” on Trust Wallet, select Bitcoin (BTC) and enter the amount in AUD. Review the transaction details before finalizing the purchase.

-

Step 4: Confirm and complete the transaction. After confirming the payment details, tap “Confirm” to complete the purchase. The Bitcoin will appear in your Trust Wallet as soon as it is finalized.

Use a non-voluntary wallet to always have your Bitcoin in your possession and optimize privacy and security.

How to buy Bitcoin in Australia on a decentralized exchange (DEX)

Buying Bitcoin on a DEX, such as Uniswap, gives you complete freedom over managing your assets. Here’s how to buy Bitcoin through a DEX:

-

Step 1: Set up a crypto wallet. Download MetaMask and create a wallet. Save the 12-word recovery phrase and put ETH in your wallet to cover transaction costs.

-

Step 2: Connect to the DEX (Uniswap). Visit the Uniswap website and click on “Connect Wallet.” Choose MetaMask or WalletConnect for mobile users.

-

Step 3: Select Bitcoin to buy. Select ETH as the token to exchange and Wrapped Bitcoin (WBTC) as the token to purchase.

-

Step 4: Review and approve the transaction. Check the details, including the ETH amount and WBTC to be received, and confirm the transaction.

-

Step 5: Confirm and complete the purchase. Once you have confirmed everything, the transaction will be processed on the Ethereum blockchain. Your WBTC will appear in your MetaMask wallet.

Using a DEX ensures you maintain control over your private keys while enjoying a decentralized trading experience.

Did you know? Bitcoin adoption in Australia has been rising recently, leading many Australians to deploy cryptocurrency to diversify their investment portfolios.

How to buy Bitcoin in Australia via P2P platforms

In Australia, you have peer-to-peer (P2P) cryptocurrency platforms such as Binance P2P to buy Bitcoin directly from other users, offering flexibility and privacy. Here’s how you can buy Bitcoin on P2P platforms:

-

Step 1: Create an account. Sign up and complete the KYC verification. Have your ID ready and verify your contact details during the process. Notably, Binance P2P, registered with AUSTRAC, ensures compliance with AML/CTF regulations, making it a reliable choice for Australians.

-

Step 2: Search for Bitcoin offers. Browse available offers, filtering by payment method (e.g., bank transfer, PayID), price or seller reputation. Prioritize sellers with high feedback scores (e.g., 95%+ positive ratings) and a history of 100+ completed trades for trustworthiness. Binance P2P displays these metrics clearly. As of 2025, Binance P2P supports over 31 fiat currencies and 700+ payment methods globally, tailoring offers to Australian users.

-

Step 3: Start a trade. Select the amount of Bitcoin or fiat currency you want to trade and click “Buy.”

-

Step 4: Make the Payment. Pay via bank transfer, PayID or another accepted payment method. The platform holds the Bitcoin in escrow until the payment is confirmed. Notably, PayID transactions are instant and free on Binance P2P, while bank transfers may take 1-2 hours. Confirm receipt with the seller via the platform’s messaging system to avoid delays.

-

Step 5: Receive your Bitcoin: Once the seller verifies your payment, the escrowed Bitcoin is released to your P2P wallet (e.g., Binance wallet). This typically happens within minutes for instant methods like PayID.

For maximum security, you could immediately transfer your BTC to a non-custodial wallet like Trust Wallet or a hardware wallet like Ledger. P2P platforms aren’t designed for long-term storage.

This P2P process offers a direct, flexible way to buy Bitcoin, with Binance P2P standing out in 2025 for its robust escrow system and wide payment options. Always double-check seller credibility and avoid off-platform payments to mitigate risks, aligning with best practices for P2P trading.

How to buy Bitcoin in Australia using Bitcoin ATMs

By using a Bitcoin ATM, you can buy Bitcoin quickly and easily. This is how:

-

Step 1: Find a Bitcoin ATM. Search for Bitcoin ATMs with CoinATMRadar. These machines are usually found in shopping centers in major Australian cities.

-

Step 2: Verify your identity. Most ATMs require a government-issued ID, such as a driver’s license or passport.

-

Step 3: Start the transaction. Select “Buy Bitcoin” and enter the amount you want to purchase in AUD or Bitcoin.

-

Step 4: Enter your wallet address. Scan the QR code of your Bitcoin wallet to enter the address so you can receive Bitcoin.

-

Step 5: Deposit the money. Deposit the money in the ATM to complete the transaction.

-

Step 6: Confirm and complete. Check the transaction and confirm the purchase. The Bitcoin will arrive in your wallet after processing.

Quick checklist for Bitcoin ATM use in Australia

-

Locate a verified ATM via CoinATMRadar.

-

Bring a pre-set wallet QR code and ID.

-

Compare fees/rates to online alternatives.

-

Use in a safe, public location.

-

Confirm receipt and track the transaction.

-

Avoid unofficial QR codes or support contacts.

-

Start with a small test transaction.

How to buy Bitcoin ETFs in Australia

Buying Bitcoin ETFs in Australia is straightforward. Just follow these steps:

-

Step 1: Choose a brokerage platform. Open an account with a brokerage that offers Bitcoin ETFs on the ASX. Make sure it complies with Australian financial regulations.

-

Step 2: Complete KYC verification. Submit proof of identity and proof of address for verification.

-

Step 3: Deposit funds. Transfer funds to your account using secure methods, such as bank transfer.

-

Step 4: Search for Bitcoin ETFs. Use the platform’s search function to find Bitcoin ETFs, such as VanEck Bitcoin ETF (VBTC) or Global X 21Shares Bitcoin ETF (EBTC).

-

Step 5: Place your order. Choose the number of units you want to buy and select a market or limit order.

-

Step 6: Confirm the purchase. Check and confirm the transaction. The ETF units will be added to your portfolio after the transaction has been completed.

Did you know: Bitcoin ETFs in Australia are scrutinized by ASIC and ASX to ensure high transparency and investor protection.

Best practices for buying Bitcoin in Australia

Store your Bitcoin securely after purchase using a reputable platform that complies with ASIC and AUSTRAC regulations. Ensure you have a secure internet connection and enable two-factor authentication (2FA).

Choose cost-effective payment methods such as bank transfers instead of credit cards. After you have purchased the Bitcoin, move it to an unsecured wallet to have complete control over your private keys.

Use a cold wallet for maximum security. Stay up to date on market trends, tax obligations, and changes in regulations to protect your investments. The crypto landscape evolves rapidly, and keeping up to date will help you make better investment decisions while ensuring compliance with Australian laws.

What are crypto payment gateways, and how do they work?

Key takeaways Crypto payment gateways enable businesses to accept cryptocurrency payments from customers. They act as intermediaries, converting crypto payments into the business’s preferred currency (crypto or fiat). Crypto payment gateways reduce transaction fees compared to traditional banking systems and provide access to a global […]

Analysis

Key takeaways

-

Crypto payment gateways enable businesses to accept cryptocurrency payments from customers.

-

They act as intermediaries, converting crypto payments into the business’s preferred currency (crypto or fiat).

-

Crypto payment gateways reduce transaction fees compared to traditional banking systems and provide access to a global customer base.

-

These gateways leverage blockchain technology to offer secure and faster transactions with fewer intermediaries, enhancing transparency and reducing the risk of fraud.

Crypto payment gateways enable businesses to accept cryptocurrency payments from customers.

They act as intermediaries, converting crypto payments into the business’s preferred currency (crypto or fiat).

Crypto payment gateways reduce transaction fees compared to traditional banking systems and provide access to a global customer base.

These gateways leverage blockchain technology to offer secure and faster transactions with fewer intermediaries, enhancing transparency and reducing the risk of fraud.

The cryptocurrency industry faces significant challenges, particularly in the area of seamless conversion between digital assets and fiat currencies. This issue makes it difficult for businesses and users to adopt cryptocurrencies for everyday transactions.

Crypto payment gateways address this need by simplifying the process of converting digital currencies into fiat, enabling smooth and efficient transactions.

This article explores what crypto payment gateways are, how these gateways work, and their pros and cons.

Cryptocurrency payment gateways, explained

A cryptocurrency payment gateway is a digital transaction facilitator that enables businesses to accept crypto payments while ensuring seamless processing and settlement.

These gateways act as intermediaries between customers who pay with digital assets and merchants who receive crypto payments, helping businesses navigate the complexities of blockchain transactions. Examples of crypto payment gateways include BitPay, Coinbase Commerce and PayPal’s crypto payment service.

One of the key advantages of using a crypto payment gateway is that businesses can receive payments in cryptocurrency while opting to convert them into fiat currency, which is then deposited into their bank accounts. This eliminates concerns about crypto price volatility while allowing merchants to offer additional payment options to their customers.

Are crypto payment gateways necessary for accepting digital currencies?

While crypto payment gateways simplify the process of accepting digital assets, they are not the only way for businesses to receive cryptocurrency payments.

Merchants can choose to accept crypto directly by using personal wallets, bypassing third-party processors. However, without a payment gateway, they would need to manually manage transactions, track payments on the blockchain, and handle currency conversion if they wish to receive fiat instead of crypto.

For businesses looking to integrate cryptocurrency payments alongside traditional methods, crypto payment gateways provide an efficient solution. These services offer real-time transaction processing, automatic conversion to fiat and additional security features that protect businesses from fraudulent transactions.

However, be aware of fees. Coinbase Commerce charges a 1% fee on all crypto payments. After your customer completes a payment, this fee is collected in the settlement currency of the transaction.

For example, if your customer makes a $250 purchase in Bitcoin (BTC), and your settlement currency is in euros, it would collect 2.5 euros (1% of the payment amount) as a fee.

Types of crypto payment gateways: Custodial vs. non-custodial

Crypto payment gateways can be classified into two main types: custodial and non-custodial. The choice between these options depends on a business’s preferences regarding security, control and ease of use.

Custodial crypto payment gateways

Custodial gateways function similarly to traditional payment processors. They receive and temporarily hold payments before allowing merchants to withdraw funds to their crypto wallets or convert them to fiat currency. This model is ideal for businesses that want a streamlined experience without dealing with direct wallet management.

Key characteristics of custodial payment gateways include:

-

Automated fiat conversion: Payments can be converted to local currency instantly, mitigating volatility risks.

-

User-friendly dashboard: Merchants can manage transactions, track payment history, and withdraw funds through an online portal.

-

Compliance features: Many custodial gateways implement Know Your Customer (KYC) and Anti-Money Laundering (AML) measures to meet regulatory requirements.

Non-custodial crypto payment gateways

Non-custodial payment gateways provide merchants with full control over their funds by immediately transferring payments to their wallets without holding them on behalf of the business. These solutions prioritize decentralization and security, allowing merchants to manage their own private keys.

Key characteristics of non-custodial payment gateways include:

-

Enhanced security: Funds are not stored by the gateway, which reduces the risk of hacks or third-party control.

-

Direct crypto transfers: Payments are sent straight to the merchant’s wallet, which eliminates withdrawal processes.

-

Greater privacy: Merchants can accept payments without undergoing extensive KYC verification.

-

Lower fees: Transaction costs are reduced for both parties since no intermediaries are involved.

-

Increased transparency: The blockchain records transactions, providing an immutable and traceable record.

-

Full control over funds: Merchants retain complete ownership and access to their crypto assets.

Did you know? Major banks and fintechs, including Bank of America, Standard Chartered, PayPal, Revolut, and Stripe, are entering the stablecoin market to enhance cross-border payments.

How do crypto payment gateways differ from traditional fiat payment gateways?

Traditional payment gateways, such as those used for credit card processing, facilitate transactions in government-issued currencies like the US dollar or euro. These fiat gateways connect a merchant’s payment system to a bank, verifying transactions based on the customer’s bank details before authorizing or declining payments.

Key distinctions between fiat and crypto payment gateways include:

-

Currency type: Fiat gateways exclusively process national currencies, whereas cryptocurrency gateways support digital assets like BTC, Ether (ETH) and stablecoins.

-

Decentralization: Traditional payment gateways rely on centralized financial institutions, while crypto payment gateways leverage blockchain technology for peer-to-peer transactions.

-

Transaction speed: Crypto payments can be settled in minutes, whereas fiat transactions, especially international payments, may take days to clear.

-

Chargeback protection: Unlike fiat payments, where chargebacks can be issued, crypto transactions are irreversible once recorded on the blockchain.

While fiat payment gateways remain essential for conventional banking transactions, crypto payment gateways are expanding payment possibilities by integrating blockchain-based financial solutions.

As cryptocurrency adoption continues to grow, businesses must evaluate their payment strategies and choose the right gateway solution that aligns with their operational needs.

Pros and cons of cryptocurrency payment gateways

You must be aware of the pros and cons of cryptocurrency payment gateways before using them, whether for business transactions or everyday personal use.

Pros of crypto payment gateways

One of the major advantages of using cryptocurrency payment gateways is the ability to settle transactions quickly. These platforms typically charge a minimal network fee (covered by the service provider) and a small service fee for customers. The streamlined process involves just one intermediary — the crypto payment processor — which enhances the user experience for both businesses and their clients.

Additionally, crypto payment systems benefit from the transparency of blockchain technology, offering protection for merchants against chargeback fraud. Unlike traditional fiat payment systems, where transactions can sometimes result in businesses not receiving the funds after they have been deducted from a customer’s account, crypto payments provide more certainty. Furthermore, these gateways can handle a variety of cryptocurrencies, mitigating the risk of market volatility for merchants.

Cons of crypto payment gateways

However, crypto payment gateways are still intermediaries in the process, meaning settlements are not fully decentralized. This centralization could pose a risk. For instance, if a crypto payment processor experiences operational disruptions, merchants may face delayed payments until the issue is resolved. Similarly, if the gateway is compromised by a cyberattack, businesses may lose access to their funds.

Another downside is that crypto payment gateways can be more expensive than direct blockchain transactions. Since these gateways act as intermediaries, they add their own fees on top of the blockchain network’s transaction costs.

As centralized entities, crypto payment processors introduce a level of trust. Merchants need to ensure that the processor is capable of offering reliable, secure services to prevent potential cyber threats.

Do cryptocurrency exchanges offer payment gateways?

Binance, Coinbase and Kraken, which are centralized cryptocurrency exchanges, provide payment gateways to facilitate crypto transactions.

Additionally, they offer application programming interfaces (APIs), which enable merchants to create custom checkout pages with full design control. APIs act as software intermediaries that allow different applications to communicate seamlessly.

Binance offers a crypto payment solution called Binance Pay, tailored for businesses that are open to accepting digital currency. Merchants can integrate Binance Pay both online and in physical stores.